< Blog

Financial statements modernisation: What will change in 2025?

From 1 January 2025, the regulation on the modernisation of financial statements will come into force, leading to a number of changes in the way French companies present their accounts. In particular, this reform aims to increase the transparency and reliability of financial information while simplifying and clarifying accounting standards.

The French Authority of Accounting Standards (Autorité des Normes Comptables) is an organisation responsible for developing and adapting the accounting rules applicable to all companies operating in France, whether public or private. Since its creation in 2009, it has supported businesses in applying these standards and contributed to the development of international accounting standards. The ANC ensures that accounting practices evolve to reflect economic and legislative changes. By ensuring that accounting practices evolve in response to economic and legislative changes, the ANC aims to improve the transparency, comparability, and relevance of financial information. This, in turn, facilitates decision-making for investors and regulators.

An example of this approach is Regulation 2022-06, adopted by the ANC on 4 November 2022. Effective from 1 January 2025, this text introduces modernised financial reporting with three main objectives:

A transfer account, similar to a rebilling, records insurance refunds or indemnities that offset all or part of an expense already recorded. While accountants frequently rely on this practice, it often complicates financial documents for non-specialists, such as bankers or company directors.

Although accountants commonly use this practice, it complicates reading financial documents for non-specialists such as bankers or company directors. As a result, the regulation eliminates expense transfer accounts (791, 796 et 797) to simplify financial reporting.

They will be replaced by revenue accounts classified by type so that a credit entry can adjust the accounts initially debited:

The regulation introduces a complete review of the concept of exceptional items, adopting a stricter definition and promoting more relevant financial information. This change marks France’s alignment with international best practice.

From now on, for an income or expense to be classified as an „exceptional item“, it must result exclusively from an event that is both significant and unusual. Otherwise, these items will be included in ordinary operating results.

This reform brings French practices closer to international standards but has significant implications:

One of the major consequences is the overhaul of fixed asset accounting schemes, notably with the elimination of accounts 675 and 775. For example, companies must now use dedicated accounts such as 657 and 757 for intangible and tangible assets.

Changes in accounting schemes for assets must be integrated into new professional routines, particularly with the elimination of accounts 675 and 775.

Asset disposals must now be recorded in the new dedicated accounts: 657 and 757 (intangible and tangible assets) or 667 and 767 (financial assets).

Account 777 is replaced by account 747 („Share of investment grants transferred to the income statement“).

The reform simplifies and standardises the presentation of financial statements, introducing major changes to their structure. Going forward:

These new formats provide a more detailed and clear structure, enabling better understanding of financial information.

The annexes to the financial statements have also been reorganised around standardised tables, making it easier to access data and navigate between the accounts and the annexes. These changes are intended to make the financial statements more readable, transparent and understandable. They will also help to improve strategic decision-making and the financial credibility of companies in the eyes of third parties.

The diversity of existing frameworks and the gradual introduction of new formats had made their use complex. To simplify, only two models will now be retained:

The Annex to the financial statements is evolving towards a standardised presentation, adapted to the type of company (size, legal status, etc.). These changes aim to harmonise presentation and information by

No major changes are anticipated.

The new regulation introduces a significant reduction of almost 20% in the accounts within the accounting plan, thereby simplifying the classification of accounting transactions. At the same time, several rules have been clarified, particularly those concerning the recognition of accrued expenses and inventory accounting.

The reform creates a clear distinction between two types of financial tables to better structure financial information:

This structure aligns with international standards, facilitating commercial and financial exchanges with foreign partners and reinforcing consistency in accounting practices.

The diversity of accounting frameworks (basic, abridged, advanced) has led to inconsistencies in the preparation of financial statements. The new regulation unifies these frameworks into a single accounting plan, distinguishing between mandatory and optional accounts.

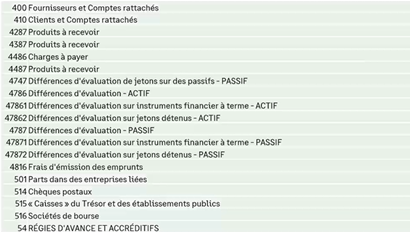

Accounts 400 (generic suppliers) and 410 (generic customers) will be eliminated in order to harmonise the accounting plan with the practices of the abbreviated system.

This reform aims to simplify the management of supplier and customer accounts, reducing complexity related to multiple frameworks and standardise their application across all accounting systems.

The reform introduces a clear distinction between mandatory and optional accounts:

This flexibility allows for customisation to meet industry-specific requirements while maintaining a standardised foundation.

The implementation of these changes in the X3 software requires several adjustments:

These changes will require updates to accounting configurations and support for teams to ensure a smooth and compliant transition.

The new accounting standards will fundamentally change business practices. To ensure a smooth transition and optimal compliance, using an integrated accounting management solution such as Sage Fiscalité is a strategic option.

These tools offer functionalities tailored to the current accounting and tax requirements, making it easier to update the accounting plan and produce financial statements.

Download the recording of our dedicated webinar ! (FR replay) To know more

In conclusion, the implementation of the regulation on the modernisation of financial statements from 1 January 2025 will be a major milestone for French companies, introducing a simplification and harmonisation of accounting practices. This reform aims to facilitate the comparison of financial statements, promote digitisation and update accounting models, while increasing the transparency and reliability of financial information.

To ensure a successful transition and compliance with these new requirements, businesses can adopt integrated accounting management solutions such as Sage Fiscalité.