< Blog

E-Invoicing in France: Agenda Updates, What's new?

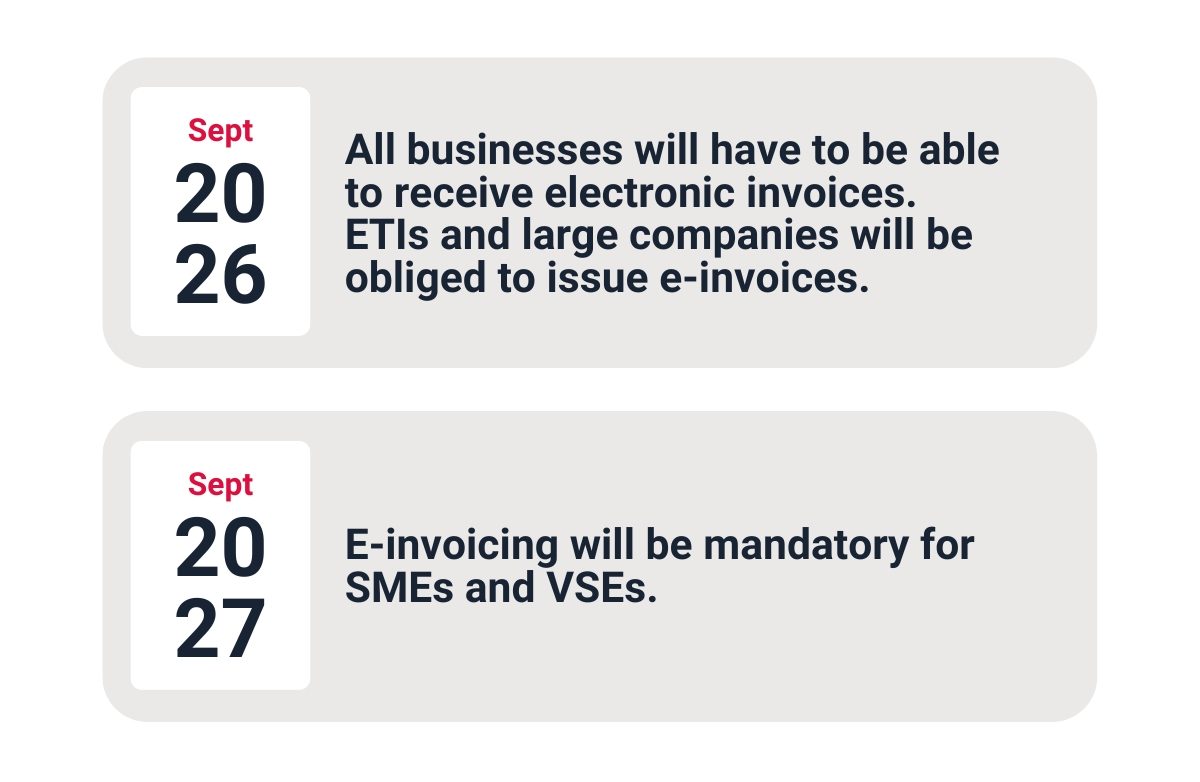

From 1 September 2026, it will no longer be possible to ask your suppliers for invoices in paper or simple PDF format. All businesses will have to:

From 1 September 2026 for the largest businesses, and progressively until September 2027 for the others, all businesses will have to:

Make sure you are compliant with four electronic invoicing methods :

It will be mandatory to archive electronic invoices in their original computer format. Archiving consists of a sealed, time-stamped deposit in a digital safe.

The creation of an invoicing network linking all BtoB players is accompanied by total transparency on the progress of each invoice, status by status:

Four obligatory statuses are communicated by all platforms:

Other statuses (made available; taken in charge; approved; partially approved; payment forwarded), which are recommended but optional, and still others, known as free statuses, will be included or not in the services offered by the platforms. These statuses are treated as management information rather than billing information. In short, customer credit management, cash flow management and business intelligence will be greatly improved.

E-reporting is the transmission of data to the tax authorities. These new data flows must be submitted:

How does it work?

The frequency of the e-reporting flows depends on the VAT regime of the company. The issuing platform chosen by the company (PPF or PDP) concentrates and transmits these flows to the tax authorities.

Do you want to know more about e-invoicing: